The bridging mortgage is primarily recognizable by its short term, mainly because this type of mortgage is used for a bridging period between purchasing a new home and selling the old one. Maatwerk-Hypotheek provides you with more information about the bridging mortgage.

Bridging mortgage: what exactly is it?

A bridging mortgage is a short-term mortgage loan intended for people who want to buy a new home before their old one has been sold. In the Netherlands, we have tax legislation that provides significant benefits when people reinvest the equity from a home into a new one. When a new home is purchased before the old one is sold, the equity from the old home effectively remains 'stuck' and cannot be invested in the new home. The bridging mortgage is designed to solve this problem.

Start my own calculation

Are you also curious about the maximum amount you could borrow to buy a home? Or do you want to know if refinancing your current mortgage would be beneficial for you? Then click on the “Start my own calculation” button below and indicate in the main menu what type of calculation (first-time buyer, mover, refinancing, mortgage based on current rental costs, or a mortgage tailored to your situation) you would like to receive. In addition to the calculation you will receive immediately, we will also send you an E-book detailing everything you need to gather to take out a mortgage. “Are”recalculate it myself" and indicate in the main menu what type of calculation you wish to receive (starter, mover, remortgaging, mortgage based on current rental costs, or a bespoke mortgage for your situation).

Besides the calculation you will receive immediately, you will also receive a E-book In addition to the calculation you will receive immediately, we will also send you an E-book detailing everything you need to gather to take out a mortgage.

A short-term loan until the transfer

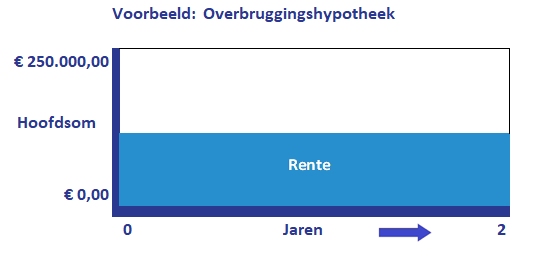

A bridging mortgage, also known as a bridging loan, does not have a term of many years, as is the case with other mortgage loans. The term is limited to a maximum of 24 months. It is therefore important that the old home is sold within this period. Once the transfer of this property is finalized at the notary, the bridging mortgage must be repaid. Can you manage without a bridging mortgage? Then this is always the better choice. This is because you will incur several costs when taking out a bridging mortgage. For instance, the interest rate on this loan is higher than on regular mortgage loans. Additionally, you must pay closing costs and notary fees, among other things.

Bridging mortgage benefits

In many situations, a bridging mortgage is a great solution. The bridging mortgage offers various benefits, such as:

- Under certain conditions, the interest is tax deductible.

- You can reduce the monthly payments with this loan.

- The equity is being released from the old house.

- You can buy a new home before the old house is sold.

Disadvantages of a bridging mortgage

To avoid double mortgage payments, a bridging mortgage can offer a solution, but this loan does not offer only advantages. There are also disadvantages to a bridging mortgage, such as:

- The interest rate is significantly higher than with regular mortgages.

- You are required to pay closing costs and notary fees.

- If the home sale takes a very long time, you may be forced to sell for a much lower home price.

- High requirements are placed on taking out this loan.

- In the event of a significantly disappointing house price, you will not be able to repay the bridging mortgage.

- You can only take out this mortgage with the mortgage lender where you also take out the mortgage for your new home.

Tax deductibility of the bridging mortgage

You therefore use the bridging mortgage exclusively to bridge the period between purchasing your new home and selling your old home. You repay the bridging mortgage in a single lump sum upon the transfer of your old home at the notary. Before that time, you can use the bridging mortgage to invest in your new home. In this way, the bridging mortgage effectively acts as an advance on the equity from your old home, which you will receive at a later date. When you repay the bridging mortgage, you are essentially only paying the interest. The interest is tax-deductible, meaning you benefit from this. This means that, generally speaking, the bridging mortgage does not have to cost you too much. Of course, you do pay a fee for taking out the bridging mortgage.

The amount of the bridging mortgage loan

You are not free to decide how much money you borrow via a bridging mortgage. The loan amount depends on the equity in your previous home, as the loan amount is adjusted accordingly. In most cases, it is possible to finance the full equity through a bridging loan when the property has already been sold but the transfer has not yet taken place. Has the property not yet been sold? Then you can often only borrow a percentage of the equity through a bridging loan.

Do take higher monthly costs into account.

A bridging mortgage allows you to invest the equity from your old home into your new home without the old home having been sold and/or transferred yet. Until the moment the old home is sold, you will therefore still have to deal with additional mortgage costs. The bridging loan does not eliminate these extra monthly costs. It is therefore important to bear in mind that monthly payments will increase until the previous home is actually sold. You will need your own savings for this. However, you can benefit from additional tax advantages. You are still entitled to mortgage interest deduction on the old mortgage, and the interest on the bridging mortgage is also tax deductible.

Mandatory to take out with the mortgage lender

Some homebuyers take out the mortgage for a new home with the same lender where they took out their previous mortgage. Others choose to take out the new mortgage with a different lender. For a bridging mortgage, this makes no difference, as it must always be taken out with the lender with whom you take out the mortgage for the new home. Therefore, you do not have a free choice in this matter.

Taking out only a bridging mortgage WITHOUT a new mortgage

In some situations, it is possible to take out only a bridging mortgage WITHOUT having to take out a new mortgage at the same time. Maatwerk-Hypotheek knows lenders who offer this option and with whom they also collaborate. This can be of interest to you in many cases if you have more than sufficient equity in your current home and plan to buy a new home where the equity exceeds the purchase price of this new home. This is the case when you have not yet sold your current home and the funds from the equity are not yet liquid in your bank account, but you do need the money already for the purchase of the new home.

Taking out a bridging mortgage during a divorce

When you are getting divorced and you own a home together with your future ex-partner, it is important that the property value is divided exactly in two parts in most cases. In this situation, taking out a bridging mortgage can be a practical choice. This may be the case when one of the partners wishes to invest their share of the equity in a new home. There are options available for this. However, a bridging loan cannot be used to buy out a (future) ex-partner.

Advice regarding the bridging mortgage

Maatwerk-Hypotheek offers you professional advice on existing mortgage types and all related mortgage matters. If you are interested in a bridging mortgage, it is important to seek sound advice beforehand. After all, you want to be sure that you are making the right choices. For thorough advice on bridging mortgages, you can always make an appointment at Maatwerk-Hypotheek. Click on the button “Request a free inventory consultation” below and leave your details so we can call or email you back. “Request a free inventory consultation” and leave your details so we can call or email you back.