The annuity mortgage, also known as the annuity mortgage, is primarily characterized by the fact that the gross monthly payments remain the same throughout the entire term. Maatwerk-Hypotheek offers you all information about the annuity mortgage.

Annuity mortgage: what exactly is it?

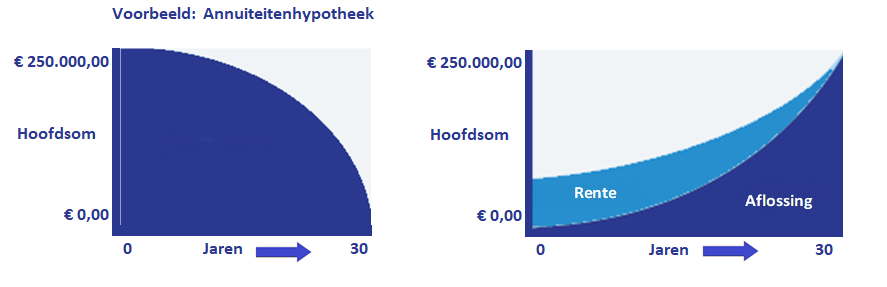

The annuity mortgage is the most popular type of mortgage since the abolition of the interest-only mortgage. When you choose an annuity mortgage, you pay a monthly amount consisting of a portion of interest and a portion of principal repayment. Grossly speaking, the monthly payment remains the same over the entire term of the mortgage. The net monthly payment increases slightly every month. This means that you start with low monthly payments and end with higher monthly payments. This relates to the ratio of the interest portion to the principal repayment portion within the total monthly payment. You are entitled to mortgage interest deduction on the interest portion, but not on the principal repayment portion.

Start my own calculation

Are you also curious about the maximum amount you could borrow to buy a home? Or do you want to know if refinancing your current mortgage would be beneficial for you? Then click on the “Start my own calculation” button below and indicate in the main menu what type of calculation (first-time buyer, mover, refinancing, mortgage based on current rental costs, or a mortgage tailored to your situation) you would like to receive. In addition to the calculation you will receive immediately, we will also send you an E-book detailing everything you need to gather to take out a mortgage. “Are”recalculate it myself" and indicate in the main menu what type of calculation you wish to receive (starter, mover, remortgaging, mortgage based on current rental costs, or a bespoke mortgage for your situation).

Besides the calculation you will receive immediately, you will also receive a E-book In addition to the calculation you will receive immediately, we will also send you an E-book detailing everything you need to gather to take out a mortgage.

Paying off increasingly more with an annuity mortgage

At the start of an annuity mortgage, the largest part of the monthly payment consists of interest. The interest portion is therefore considerably larger than the principal repayment portion. You repay relatively little principal, but you pay a lot of interest. You are entitled to mortgage interest deduction on the interest portion, allowing you to benefit significantly from this. During the term of the annuity mortgage, the interest portion becomes progressively smaller and the principal repayment portion progressively larger. This means that the amount on which you benefit from mortgage interest deduction decreases, resulting in rising monthly payments. Maatwerk-Hypotheek can advise you. We can assess whether an annuity mortgage is truly the best fit for you.

Annuity mortgage benefits

The annuity mortgage is currently the most popular type of mortgage, and not without reason. The annuity mortgage offers various interesting benefits, such as:

- You are entitled to a maximum of 30 years of mortgage interest deduction.

- At the end of the term, the mortgage is fully paid off.

- The mortgage debt decreases over the term.

- The mortgage interest rate is lower than with interest-only mortgage types.

Disadvantages of annuity mortgage

The annuity mortgage also has some disadvantages to take into consideration. The main disadvantages are:

- The net monthly costs increase over the term.

- The repayment portion is relatively small for a long time.

- With a term of 30 years, you will have paid off only half of the mortgage debt after an average of 22 years.

- You will benefit less and less from mortgage interest deduction over the term.

The mortgage debt is decreasing relatively slowly.

With an annuity mortgage, the ratio between the interest portion and the principal repayment portion within the monthly payment changes constantly. By default, the interest portion decreases and the principal repayment portion increases. Because the interest portion decreases, you benefit less and less from mortgage interest deduction. The principal repayment portion increases, meaning you pay off the mortgage debt increasingly quickly. The smaller the remaining mortgage debt, the less interest you pay. If you have a term of 30 years, it takes an average of 22 years to pay off the first half of the mortgage debt. You therefore pay off the second half in the last 8 years of the mortgage term. These are the years in which the interest portion is smallest.

The annuity mortgage is fully repaid within the term.

An important advantage of the annuity mortgage is that the mortgage debt is fully repaid within the term. You start repaying the mortgage debt from the very first month, although this is a relatively small monthly amount at the start. Consequently, the risk of your home becoming underwater is small when you choose an annuity mortgage. The interest portion, for which you are entitled to mortgage interest deduction, decreases. As a result, you receive less and less back from the tax authorities, causing the net monthly cost to increase. Consequently, the net monthly costs of the annuity mortgage continue to rise. With a linear mortgage, this works exactly the other way around.

Seek advice on the annuity mortgage.

The annuity mortgage is currently the most popular type of mortgage, but that does not necessarily mean it is the right choice for you. It is therefore always advisable to seek proper advice. You are, of course, always welcome at Maatwerk-Hypotheek for this. We advise you on an independent basis, ensuring you are making the truly right choice. You can make an appointment immediately for personal advice regarding the annuity mortgage.

Personal advice on the annuity mortgage

Would you like to know more about annuity mortgages, or do you have this type of mortgage and want to limit the risks? Maatwerk-Hypotheek is happy to assist you. You are most welcome to visit us for personal advice, even if you wish to refinance or transfer your mortgage. Click on the “Request free consultation” button below and leave your details so we can call or email you back. “Request a free inventory consultation” and leave your details so we can call or email you back.