You can recognize the bank savings mortgage by the fact that a blocked savings account is linked to the mortgage, whereby a savings amount is built up over the term. Maatwerk-Hypotheek provides you with more insight into the bank savings mortgage.

Bank savings mortgage: what exactly is it?

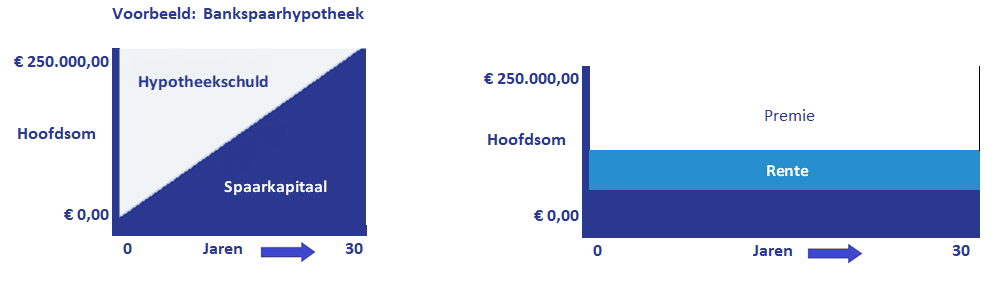

The bank savings mortgage is an interest-only mortgage. With interest-only mortgages, the right to mortgage interest deduction lapses. Therefore, with a bank savings mortgage, no principal is repaid on the mortgage debt during the mortgage term; instead, an amount is saved in a blocked savings account during this period. Ultimately, the mortgage must be repaid with this accumulated amount.

Start my own calculation

Are you also curious about the maximum amount you could borrow to buy a home? Or do you want to know if refinancing your current mortgage would be beneficial for you? Then click on the “Start my own calculation” button below and indicate in the main menu what type of calculation (first-time buyer, mover, refinancing, mortgage based on current rental costs, or a mortgage tailored to your situation) you would like to receive. In addition to the calculation you will receive immediately, we will also send you an E-book detailing everything you need to gather to take out a mortgage. “Are”recalculate it myself" and indicate in the main menu what type of calculation you wish to receive (starter, mover, remortgaging, mortgage based on current rental costs, or a bespoke mortgage for your situation).

Besides the calculation you will receive immediately, you will also receive a E-book In addition to the calculation you will receive immediately, we will also send you an E-book detailing everything you need to gather to take out a mortgage.

The bank savings mortgage and the savings mortgage

The bank savings mortgage is fundamentally very comparable to the savings mortgage, but there are important differences. With a bank savings mortgage, a free savings account is used to build up capital. In the case of a savings mortgage, this amount is built up in an insurance policy, which is generally expensive. As a rule, this makes the savings mortgage more expensive than the bank savings mortgage. Another important difference, however, is that a term life insurance policy is always included with a savings mortgage. This is not the case with the bank savings mortgage. This means that the premium for the term life insurance is added on top of the monthly payments.

The monthly payments of the bank savings mortgage

The monthly payments you have to make on a bank savings mortgage are divided into two parts. Firstly, you pay mortgage interest. This amount remains the same throughout the entire fixed-interest period, giving you full control over it. The second part is the savings portion. This portion is placed in a blocked savings account, thereby building up capital to pay off the mortgage at the end of the term. With this, you have a full guarantee that sufficient capital will be built up to actually make the full repayment. The interest you receive on the savings amount is equal to the mortgage interest you have to pay.

Bank savings mortgage benefits

The bank savings mortgage offers several interesting advantages compared to other types of mortgages, especially for people who took out this type of mortgage before 2013:

- Maximizing the benefit of mortgage interest deduction (when taken out before 2013)

- The final amount is fully guaranteed.

- Hardly any higher monthly costs when mortgage interest rates rise

Disadvantages of a bank savings mortgage

The bank savings mortgage falls under interest-only mortgages, which have not been permitted to be granted since 2013 due to the high risks. It therefore goes without saying that the bank savings mortgage has various disadvantages:

- Switching to another mortgage lender is not easy.

- Due to new mortgage rules, there is no longer an entitlement to mortgage interest deduction.

- For wealth accumulation and borrowing, you are tied to one party.

- The tax rules are very strict.

- You do not make any repayments during the term of the mortgage.

- Costs for term life insurance are in addition to the expenses.

- The interest rate may turn out to be higher compared to other types of mortgages.

The bank savings mortgage is not available to everyone.

Not everyone can opt for a bank savings mortgage. This type of mortgage can be taken out by people who already had a mortgage before 2013. Consequently, first-time buyers cannot take out a bank savings mortgage. This is also a very disadvantageous choice, as the right to mortgage interest deduction for the bank savings mortgage also ceased to exist as of January 1, 2013. If one wishes to increase the bank savings mortgage, this is only possible by means of a linear or annuity mortgage, requiring monthly repayments. A minimum term of 15 or 20 years applies to taking out a bank savings mortgage. The return is taxed progressively if the bank savings mortgage is terminated within this period. Maatwerk-Hypotheek can help you clarify matters through sound mortgage advice.

Mortgage advice on the bank savings mortgage

Do you have a bank savings mortgage and would you like to increase, convert, or perhaps refinance it? Maatwerk-Hypotheek would be happy to check your specific options. We will examine the most advantageous options for you, both now and in the future. You can make an appointment with us for personal mortgage advice regarding the bank savings mortgage. Click on the button “Request a free inventory consultation” below and leave your details so we can call or email you back. “Request a free inventory consultation” and leave your details so we can call or email you back.