The life mortgage is best recognized by the fact that a certain sum is built up over the term using a life insurance policy. Maatwerk-hypotheek tells you everything about the life mortgage.

Life insurance mortgage: what is it exactly?

The life mortgage is one of the mortgage types that falls under interest-only mortgages. This means that with a life mortgage, you do not repay the mortgage debt during the term of the mortgage. Instead, an amount is built up by paying premiums for a life insurance policy. This amount can be used to pay off the mortgage at the end of the term. An additional advantage is that a term life insurance policy is linked to the life insurance. Should you die prematurely, the remaining mortgage debt will be paid off with this term life insurance. With a life mortgage, one can choose to build up capital through interest, but also by investing in investment funds. The amount built up during the mortgage period therefore depends on the investment result, if investing has been chosen. Compared to other mortgage types, the life mortgage is reasonably comparable to a savings mortgage, with the difference that here, one can also choose to build up capital through investments.

In addition, the advantage is that if you terminate your existing endowment mortgage, the life insurance policy can potentially be continued with a new mortgage lender or solely as a separate term life insurance policy.

Start my own calculation

Are you also curious about the maximum amount you could borrow to buy a home? Or do you want to know if refinancing your current mortgage would be beneficial for you? Then click on the “Start my own calculation” button below and indicate in the main menu what type of calculation (first-time buyer, mover, refinancing, mortgage based on current rental costs, or a mortgage tailored to your situation) you would like to receive. In addition to the calculation you will receive immediately, we will also send you an E-book detailing everything you need to gather to take out a mortgage. “Are”recalculate it myself" and indicate in the main menu what type of calculation you wish to receive (starter, mover, remortgaging, mortgage based on current rental costs, or a bespoke mortgage for your situation).

Besides the calculation you will receive immediately, you will also receive a E-book In addition to the calculation you will receive immediately, we will also send you an E-book detailing everything you need to gather to take out a mortgage.

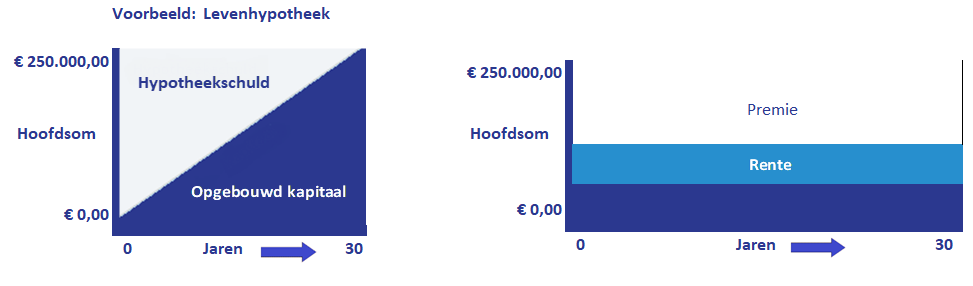

The monthly payments for the endowment mortgage consist of two parts.

The monthly costs associated with a life mortgage consist of two parts. Firstly, there is an interest component. This is the interest you pay on the outstanding mortgage debt, which remains constant for the entire term. Secondly, you pay a premium portion for the term life insurance linked to your life mortgage. The other option is to choose to invest in your life mortgage. In this case, you deposit a monthly amount into your investments and also pay a premium for the linked term life insurance.

Life mortgage benefits

The Life Mortgage offers several advantages over other types of mortgages. You can count on the following benefits, among others:

- Flexibility: you are not tied to one mortgage lender

- Low monthly costs

- Your tax benefit is maximized

Disadvantages of life mortgage

Of course, there are also some disadvantages to the endowment mortgage, and these certainly should not be forgotten. There are various important disadvantages, such as:

- It is not guaranteed that you will build up sufficient capital for full repayment of your endowment mortgage.

- In the event of a low return, the monthly deposit increases.

- A new life insurance mortgage has hardly been offered by lenders since 2013.

- The costs of term life insurance are relatively often high.

Redeeming or paying out a life mortgage

Previously, it was virtually impossible to choose to cash out a life mortgage or surrender an investment mortgage without financial loss. Substantial penalties were imposed by the tax authorities for extra repayments and in the event of a cash-out. This rule was abolished as of April 2017, making it now more advantageous and easier to make extra repayments on a life mortgage. Until April 2017, there was also a rule requiring the life mortgage to remain untouched for at least 15 or 20 years. This rule has also been dropped, making refinancing a life mortgage easier. However, this does not mean that it is a financially smart choice. Maatwerk-Hypotheek would be happy to advise you.

Converting a life mortgage

Converting your life insurance mortgage is possible in practice, but here too, it is not always advisable. In certain cases, it is financially more advantageous to make extra repayments on the mortgage than to convert it. Due to disappointing returns, resulting in high monthly contributions, many people wish to convert their life insurance mortgage. In this case, you will incur several costs. If the fixed-rate period has not yet expired, you may also have to pay a substantial amount in penalty interest. Maatwerk-Hypotheek can calculate for you whether it is financially beneficial to convert your life insurance mortgage. We can also assess which type of mortgage would be best suited for you to convert your mortgage to.

Converting a life insurance mortgage into a savings mortgage

There are people with an endowment mortgage who wish to convert this mortgage into a savings mortgage. It is important to know that the return on savings is often lower than the return on investments. On the other hand, with a savings mortgage, you can save at an interest rate equal to the mortgage interest you pay. While the risk of the endowment mortgage can be reduced by converting it to a savings mortgage, this conversion does not always yield benefits. Furthermore, it is not always possible. Maatwerk-Hypotheek would be happy to review your options.

Converting a life mortgage to reduce the risks

Do you want to convert your endowment mortgage to minimize the risks as much as possible? In general, it is a better option to convert the mortgage into a linear or an annuity mortgage. With these two types of mortgages, you start paying off the mortgage debt from the very beginning, significantly reducing the risk of residual debt. However, your monthly payments will increase, as you have to pay both an interest portion and a principal repayment portion each month. Because you start paying off the mortgage immediately with one of these two types, the risk of your home becoming underwater is much smaller.

Refinancing a life mortgage involves costs.

Surrendering or refinancing a life mortgage is possible, but in certain cases entails considerably high costs. In this instance, it can be described as a usurious policy. The policy is terminated, and any costs not yet charged will be deducted in a single lump sum. This is subsequently offset against the policy value. The mortgage lender charges fees, which are often high, meaning you only receive the remaining value of the policy. Consequently, the surrender value is significantly lower than the sum of the premiums you have paid and any potential return. Financially, this can therefore be significantly disadvantageous. Naturally, Maatwerk-Hypotheek can advise you.

Making the life mortgage premium-free

Making a life insurance policy premium-free means that you stop paying premiums, but you do not surrender the policy.

The insurance then continues up to and including the original end date, but with lower insured amounts. You can still choose to surrender this insurance at a later date. The advantage of this may be that the premiums paid still generate a return until the end of the term.

If a life insurance policy is made premium-free, the accumulated value will be used as a lump sum for a comparable policy. The insured benefits will be lower.

Save yourself to pay off the life insurance mortgage

The endowment mortgage is a type of interest-only mortgage. This means that the mortgage debt only needs to be repaid at the end of the term. When you surrender the endowment mortgage, it is up to you to find an alternative solution for building wealth. After all, it is important that you have built up sufficient capital by the end of the mortgage term to repay the mortgage. It is not always possible to take out a new mortgage for the same amount. You are, after all, older and perhaps already retired. This reduces the maximum mortgage amount, which may force you to sell the home if you are unable to secure a new mortgage for the required amount. There are several ways you can ensure the necessary capital accumulation yourself. Maatwerk-Hypotheek is happy to think along with you.

Refinancing the life mortgage

Many people want to switch their endowment mortgage to another type to limit the risks. For example, many people want to switch their endowment mortgage to a bank savings mortgage. In this case, it is important to know that the guaranteed final amount may not exceed the amount of the original deposit for the endowment mortgage. Additionally, there are many people who want to switch their endowment mortgage to an annuity mortgage or a linear mortgage. With these mortgage types, you are entitled to mortgage interest deduction. Furthermore, you start repaying the mortgage debt immediately. Maatwerk-Hypotheek is happy to advise you and review the best options for you together with you.

Take a fine into account

Are you planning to refinance your life insurance mortgage for financial benefit? Then do not forget that it is quite possible you will have to pay a penalty for the refinancing. This penalty can wipe out the financial benefit. The amount of the penalty is not fixed. This depends on several factors, such as the amount of the mortgage debt, the mortgage interest rate, and the remaining fixed-rate period. The longer the fixed-rate period is valid, the higher the penalty. The penalty you ultimately have to pay is, however, tax-deductible. Maatwerk-Hypotheek can, of course, tell you more about this.

Seek advice on the life insurance mortgage

Do you have an endowment mortgage and would you like to know if refinancing is beneficial for you? Are you curious about the best steps to take regarding your endowment mortgage? Maatwerk-Hypotheek is ready to assist you with independent mortgage advice. You can schedule an appointment immediately for professional advice on endowment mortgages. Click on the button “Request a free inventory consultation” below and leave your details so we can call or email you back. “Request a free inventory consultation” and leave your details so we can call or email you back.